Most Canadian investors are getting advice that does not fit their goals. Financial advisors sell what they are paid to sell. National headlines paint the whole country with one number. And smaller real estate markets often sell on cash flow alone, since it is the easiest number to show buyers.

That leaves many new investors thinking cash flow in a secondary market is the only way to win in real estate. It is not the only way. In this post, we will walk through where this advice falls short, and how to actually compare your options before you invest.

Why Financial Advisor Advice Often Falls Short

A lot of financial advisors push mutual funds with high fees, sometimes over 2 percent a year. That fee structure is part of how they get paid, so it shapes what they recommend.

Low-cost ETFs can do the same job for a fraction of the cost. Before we go further, we should be upfront. We sell real estate, and we are biased, especially toward Toronto multiplexes. We back what we sell, and we have real money in these deals too.

We are not telling you to put everything into real estate either. Most people should diversify. Mutual funds carry high fees, ETFs are usually the better option for that part of a portfolio, and the right type of physical real estate tends to net better returns than a real estate fund. Real estate is just less passive, and it needs more capital upfront, so you need to be ready for that financially and practically.

Is Your Home Really Your Best Investment?

A lot of people will tell you your home is not an investment. We would say it depends. A home comes with things you cannot put a price on, like schools or the community you want to live in. Sometimes that makes it a weaker investment on paper compared to other options.

But for most Canadians, their home actually is their best investment so far. The gains are tax free, and it builds wealth just by living in it.

If you want to scale into more properties, your home alone will not get you there. A home is pure debt with no income behind it, which makes it harder to qualify for more borrowing. An investment property that covers its own debt and expenses makes it easier to qualify for your next mortgage. The order you buy in matters. Investing first and buying your own home after can open up more properties down the line compared to doing it the other way around.

Why National Headlines Do Not Tell the Full Story

Be careful what you read and where it is coming from. Not all neighbourhoods or types of homes move the same way. Markham behaves differently than Riverdale. Toronto condos perform very differently than Toronto semis. One number for the whole city will not tell you what is happening on the specific house you want to buy or sell.

A lot of headlines also compare this month’s data to a year ago. Year over year numbers can still show prices coming down, even while prices have actually been recovering since the start of the year if you look more closely.

If you are only watching the news for your real estate decisions, you are probably behind. Following local market updates on the areas you actually care about gives you a more accurate read than a national headline ever will.

Cash Flow Versus Value-Add, by the Numbers

Cash flow versus value-add trips up a lot of investors. Neither one is better. It depends on what you actually want.

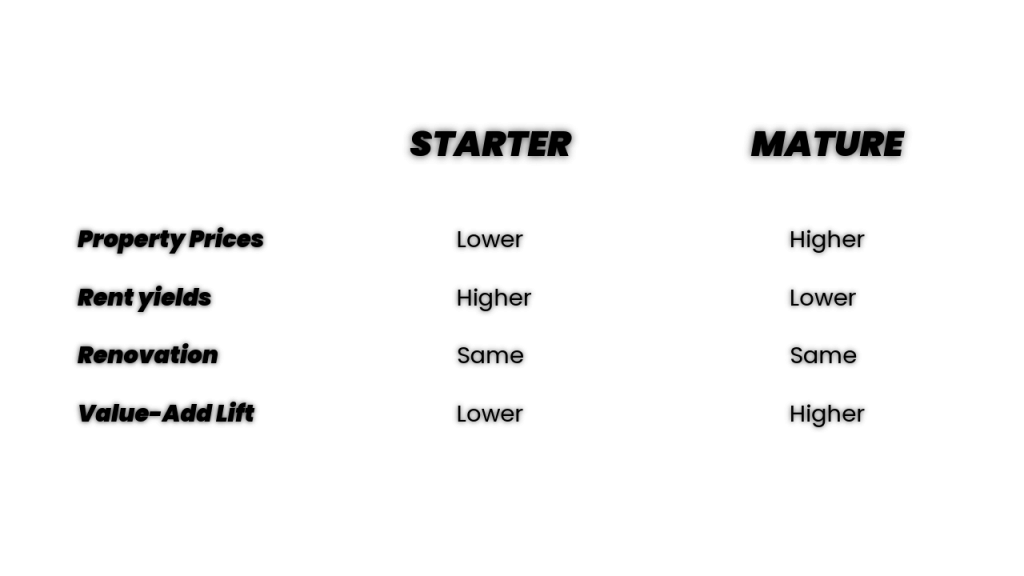

Secondary markets often get sold on cash flow because it is the easiest number to show, and lower purchase prices attract a bigger pool of buyers looking for extra income now. That is a real strategy, but it is not the whole story if your goal is to maximize returns. If you are taking on a value-add project, those cheaper markets usually are not your best move, since lower property values mean a smaller price gap to capture after renovation.

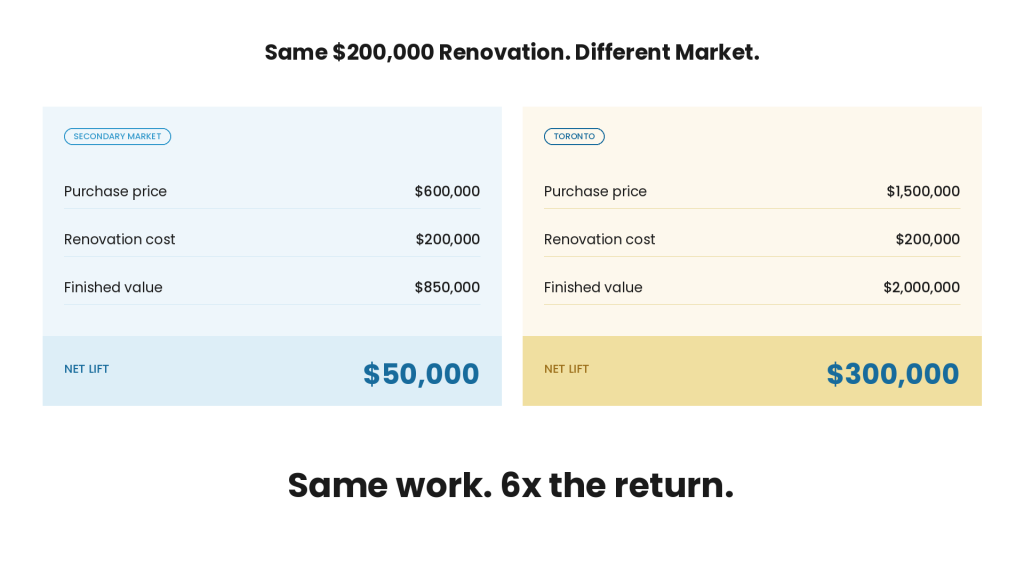

Here is what that looks like in real numbers. Buy a property in a secondary market for $600,000, put in $200,000 in renovations, and the finished value comes in at $850,000. After renovation costs, that is a $50,000 lift. Now take that same $200,000 renovation and put it into a Toronto property. Buy for $1.5 million, finish at $2 million, and after renovation costs, that is a $300,000 lift. Same renovation budget, same work, six times the return, just because of where it happened.

Which Strategy Actually Fits Your Goals?

A property that pays an extra $1,000 a month works out to $12,000 a year. To catch up to a $300,000 value-add lift, you would need over 20 years of that cash flow. The value-add project did it in about six months.

That does not mean cash flow or secondary markets are wrong. They answer a different question than value-add does. If your goal is cash flow and you have limited capital, a secondary market can make sense. If your goal is maximum return and you are ready for a renovation project, a market like Toronto often gives you a bigger lift for the same amount of work.

The real problem is advice that never asks what you are actually trying to achieve. The right answer depends entirely on your goal, not on which strategy is trending.

Let’s Find the Right Strategy for You

Cash flow and value-add are not competing strategies. They are answers to two different questions, and the right one depends on your goals, your capital, and how hands-on you want to be. Working with a team that asks the right questions first makes that decision a lot clearer.

Our brokerage specializes in Toronto multiplexes. We’ll help you find deals, crunch the numbers, and guide you through renovations and management. If you want full support in Toronto multiplex investing, our team can help you:- Find high-potential properties

- Crunch the numbers so you know exactly where you stand

- Coach you through renovations to maximize returns

- Lock in great tenants

- Provide full property management so your investment runs smoothly

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.