If you’re analyzing rental property in Toronto, you need to understand cap rates properly.

As of 2026, typical Toronto cap rates look like this:

- Condos: ~3.5%

- Single-family rentals: ~4%

- Small multiplexes: 5% to 5.5%

- Commercial multi-family: ~4.5%

- Garden and laneway suites: 8%+ depending on build cost

Those numbers determine whether a property cash flows, whether you can refinance after renovations, and whether you are buying a deal or simply overpaying.

Most investors misunderstand cap rates because they use purchase price instead of stabilized market value. That mistake alone can destroy returns.

This guide breaks down how Toronto cap rates actually work, what qualifies as “good,” and how multiplex investors use them to build equity safely.

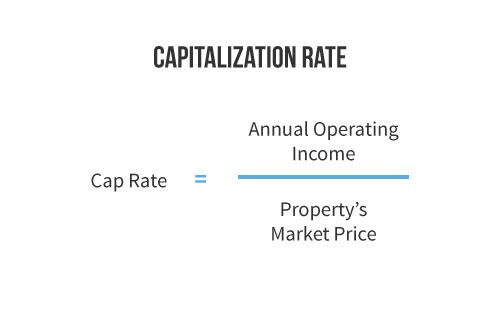

What Is Cap Rate?

Cap rate, short for capitalization rate, measures the return a property generates based strictly on its income.

It ignores mortgage financing. It focuses only on the property itself.

The formula is simple:

Cap Rate = Net Operating Income (NOI) ÷ Current Market Value

Net Operating Income equals rental income minus operating expenses, including:

- Property taxes

- Insurance

- Utilities paid by landlord

- Maintenance and repairs

- Property management

- Vacancy allowance

Mortgage payments are not included.

That is intentional. Cap rate evaluates the asset, not your financing.

How is Cap Rate Calculated?

Key Things to Know About Cap Rates

- No Appreciation Factored In: Cap rate only looks at rental income. If you want a full picture, you also need to consider long-term appreciation.

- Mortgage Isn’t Included: Cap rate ignores mortgage payments, which affects your cash flow and risk.

- Use Market Value, Not What You Paid: Always base your cap rate on the property’s current value—not your purchase price.

- After-Reno Numbers Count: When renovating, don’t just add the cost of renos to the price. Use the real after-renovation market value to avoid fooling yourself with fake high cap rates.

So yes—cap rate is helpful, but it’s not the full story. It’s just one piece of your investment puzzle.

What Is a Good Cap Rate in Toronto in 2026?

A “good” Toronto cap rate depends on property type, location, and risk tolerance.

Here’s how it typically breaks down:

| Property Type | Typical Toronto Cap Rate |

|---|---|

| Condo | ~3.5% |

| Single-Family Rental | ~4% |

| Small Multiplex | 5–5.5% |

| Commercial Multi-Family | ~4.5% |

| Garden / Laneway Suite | 8%+ |

For most Toronto multiplex investors, we target at least 5% to create breathing room for financing costs and unexpected repairs.

Lower than that and you’re relying heavily on appreciation.

Higher than that usually means more risk, heavier renovation, or weaker location.

Why Toronto Cap Rates Are Lower Than Other Cities

Toronto cap rates are lower than many secondary markets for one reason: demand.

Strong population growth, limited land supply, stable rental demand, and long-term appreciation compress yields.

You are trading higher immediate yield for:

- Stronger long-term appreciation

- Higher liquidity

- Lower vacancy risk

- Better refinance potential

If you want 8–10% cap rates, Toronto is not the market.

But if you want stable income with long-term upside, Toronto multiplex properties remain competitive.

Real Toronto Multiplex Example

Let’s look at a practical example.

Scenario 1: Turnkey Property

- Purchase price: $1,100,000

- Annual NOI: $55,000

- Cap rate: 5%

Straightforward. Now compare that to a value-add deal.

Scenario 2: Renovation Strategy

- Purchase: $800,000

- Renovations: $150,000

- Total cost: $950,000

- Annual NOI after renovations: $55,000

- Cap rate: 5.8%

At a 5% market cap rate, that $55,000 NOI supports a value of $1,100,000. You created roughly $150,000 in equity.

Here’s the math investors forget:

At a 5% cap rate, every $10,000 increase in NOI adds $200,000 in property value.

That’s why value-add strategies matter.

What Is Cap Rate?

Cap rate, short for capitalization rate, measures the return a property generates based strictly on its income.

It ignores mortgage financing. It focuses only on the property itself.

The formula is simple:

Cap Rate = Net Operating Income (NOI) ÷ Current Market Value

Net Operating Income equals rental income minus operating expenses, including:

- Property taxes

- Insurance

- Utilities paid by landlord

- Maintenance and repairs

- Property management

- Vacancy allowance

Mortgage payments are not included.

That is intentional. Cap rate evaluates the asset, not your financing.

How is Cap Rate Calculated?

Key Things to Know About Cap Rates

- No Appreciation Factored In: Cap rate only looks at rental income. If you want a full picture, you also need to consider long-term appreciation.

- Mortgage Isn’t Included: Cap rate ignores mortgage payments, which affects your cash flow and risk.

- Use Market Value, Not What You Paid: Always base your cap rate on the property’s current value—not your purchase price.

- After-Reno Numbers Count: When renovating, don’t just add the cost of renos to the price. Use the real after-renovation market value to avoid fooling yourself with fake high cap rates.

So yes—cap rate is helpful, but it’s not the full story. It’s just one piece of your investment puzzle.

What Is a Good Cap Rate in Toronto in 2026?

A “good” Toronto cap rate depends on property type, location, and risk tolerance.

Here’s how it typically breaks down:

| Property Type | Typical Toronto Cap Rate |

|---|---|

| Condo | ~3.5% |

| Single-Family Rental | ~4% |

| Small Multiplex | 5–5.5% |

| Commercial Multi-Family | ~4.5% |

| Garden / Laneway Suite | 8%+ |

For most Toronto multiplex investors, we target at least 5% to create breathing room for financing costs and unexpected repairs.

Lower than that and you’re relying heavily on appreciation.

Higher than that usually means more risk, heavier renovation, or weaker location.

Why Toronto Cap Rates Are Lower Than Other Cities

Toronto cap rates are lower than many secondary markets for one reason: demand.

Strong population growth, limited land supply, stable rental demand, and long-term appreciation compress yields.

You are trading higher immediate yield for:

- Stronger long-term appreciation

- Higher liquidity

- Lower vacancy risk

- Better refinance potential

If you want 8–10% cap rates, Toronto is not the market.

But if you want stable income with long-term upside, Toronto multiplex properties remain competitive.

Real Toronto Multiplex Example

Let’s look at a practical example.

Scenario 1: Turnkey Property

- Purchase price: $1,100,000

- Annual NOI: $55,000

- Cap rate: 5%

Straightforward. Now compare that to a value-add deal.

Scenario 2: Renovation Strategy

- Purchase: $800,000

- Renovations: $150,000

- Total cost: $950,000

- Annual NOI after renovations: $55,000

- Cap rate: 5.8%

At a 5% market cap rate, that $55,000 NOI supports a value of $1,100,000. You created roughly $150,000 in equity.

Here’s the math investors forget:

At a 5% cap rate, every $10,000 increase in NOI adds $200,000 in property value.

That’s why value-add strategies matter.

How To Make A Multiplex In Toronto: Your Complete Guide!

Cap Rate and Refinance Strategy

Cap rate directly affects your refinance potential.

If you increase NOI and the market cap rate remains stable, your property value rises proportionally.

Higher value allows:

- Cash-out refinance

- Capital recycling

- Portfolio scaling

- Risk reduction

Low cap rate properties, especially condos, leave little margin for error.

Multiplex properties provide more room to increase income and stabilize returns.

Cap Rate vs Interest Rates

Cap rates and interest rates often move in the same direction.

When borrowing costs rise, investors demand higher yields. That pushes cap rates upward.

As of 2026, interest rates have moderated while many cap rates have not fully adjusted. That creates selective opportunities for disciplined buyers.

But cap rate alone does not guarantee cash flow.

You still need to stress-test financing properly.

Common Cap Rate Mistakes Toronto Investors Make

- Using purchase price instead of current market value

- Ignoring vacancy allowance

- Forgetting maintenance reserves

- Overestimating post-renovation rent

- Confusing cap rate with cash-on-cash return

Cap rate is one tool. Not the full analysis.

FAQs About Toronto Cap Rates

Is 5% a good cap rate in Toronto?

For small multiplex properties, 5% is generally considered a solid starting point in 2026.

Why are Toronto cap rates lower than other cities?

Higher demand, land scarcity, and long-term appreciation compress yields.

Are multiplex cap rates higher than condos?

Yes. Multiplex properties typically trade 1–2% higher than condos due to stronger rental income relative to price.

Do cap rates include mortgage payments?

No. Cap rate evaluates property income before financing.

Can I increase cap rate through renovations?

Yes. Increasing NOI through value-add strategies raises effective yield and can increase property value if market cap rates hold.

Final Thoughts: How Toronto Investors Should Use Cap Rates

Cap rate is not just a metric.

It determines:

- Whether your property cash flows

- Whether you can refinance

- Whether you’re buying at fair value

- Whether your downside risk is manageable

In Toronto, small multiplex properties in the 5–5.5% range currently offer the strongest balance between income and stability.

If you are evaluating a Toronto duplex, triplex, or garden suite and want to model whether the cap rate actually works at today’s financing conditions, book a strategy session with us and we’ll walk through the numbers properly.

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.