Most people assume Toronto multiplexes are out of reach. The price tags look intimidating, the market sounds expensive, and the whole thing feels like it’s for someone with much deeper pockets. That assumption stops a lot of good investors before they even get started.

The honest number to get into a cash-flowing Toronto multiplex in a starter neighbourhood right now is around $250,000 all in. That covers your down payment and closing costs on the right property. And depending on the path you choose, there is actually a way to pull a big chunk of that money back out a few months after you close. Here is exactly how it works.

The Two Paths Into a Toronto Multiplex

There are two main ways to get into a Toronto multiplex, and the capital required is different for each one. Understanding the difference before you start looking at properties will save you a lot of confusion.

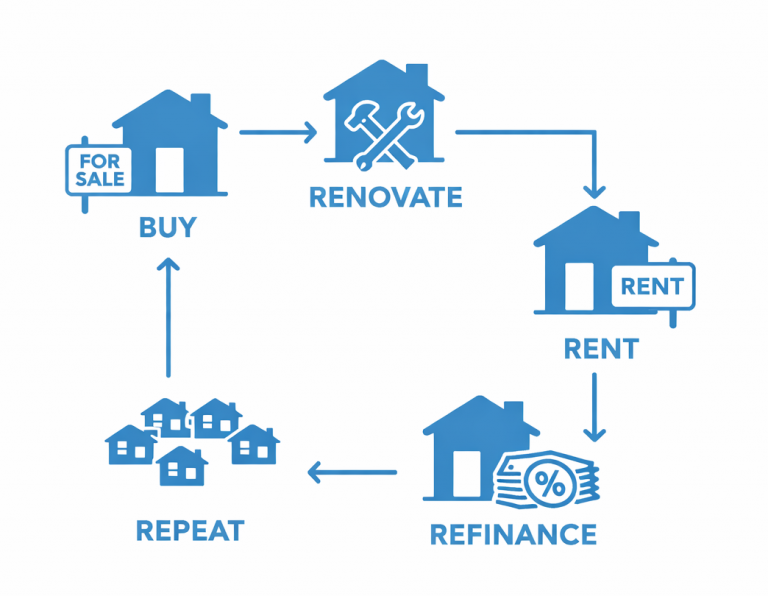

The first is a turnkey. You buy a property that already has separate units, already has tenants in place, and already generates rent from day one. You close, collect rent, and the property starts paying for itself immediately. No renovation projects, no waiting months before income starts. This is the simplest entry point and the right starting place for most investors.

The second is a value-add project. You buy a property that needs work, renovate it to add or improve units, rent it out, and end up with a property worth more than what you put in. The purchase price is lower, but the total cost is higher upfront because you are adding renovation costs on top of your down payment and closing costs. The payoff is that you can refinance after the renovation and pull a significant portion of your capital back out.

What a Turnkey Deal Actually Costs

In starter Toronto neighbourhoods, turnkey multiplexes are running close to $1 million right now. With a 20% down payment plus closing costs, you are looking at roughly $250,000 total out of pocket. The bank finances the remaining $750,000 to $800,000, provided you can qualify with strong enough income.

Here is a real example from our current brokerage listings. Three units, all rented. Purchase price of $1.1 million. Approximately $250,000 out of pocket. After all expenses including the mortgage are paid, there is around $1,600 left over every single month. Your tenants are covering the mortgage. You are not paying out of your own pocket each month to hold the property.

That positive monthly cash flow is the foundation of why Toronto multiplexes work as an investment. You are building equity in a property, in one of Canada’s most supply-constrained cities, without it costing you anything out of pocket month to month. To understand how to evaluate that return more precisely, our total return calculator can help you model the full picture including appreciation, mortgage paydown, and cash flow together.

How Value-Add Projects Change the Math

Value-add projects look cheaper at first because the purchase price is lower. Lately properties suitable for this strategy have been coming up for under $900,000. But the renovation budget changes the total picture quickly. If a property needs $150,000 in work before it is ready to rent, you are now looking at roughly $360,000 total between down payment, closing costs, and renovation costs. That is more money upfront than a turnkey deal.

The reason investors take this path is what happens after the renovation. Once the work is done and the units are rented, the property is worth more than what you put in. In this example, say the finished property appraises at $1.1 million. You refinance, the bank lends you 80% of that value, which is $880,000. Your original loan was $720,000. The bank gives you $160,000 back. Your total capital stuck in the deal drops from $360,000 down to around $200,000. Same monthly rent and cash flow. Just less of your own money tied up in the property long term.

Find an even better deal and the numbers shift further. A property purchased for $800,000 needing $200,000 in renovations costs $390,000 upfront. If it appraises at $1.1 million after the renovation, the refinance returns $240,000. Now you only have about $150,000 of your own money left in the deal. Because you have less capital tied up while generating the same rent, your return on invested capital goes up considerably. This is the core logic behind why experienced investors often prefer value-add opportunities despite the added complexity.

Turnkey vs. Value-Add — A Side-by-Side Look

Here is a straightforward comparison of both paths based on the numbers above.

| Turnkey | Value-Add (Example A) | Value-Add (Example B) | |

|---|---|---|---|

| Purchase price | $1,100,000 | $900,000 | $800,000 |

| Renovation cost | $0 | $150,000 | $200,000 |

| Total upfront capital | ~$250,000 | ~$360,000 | ~$390,000 |

| Post-renovation value | $1,100,000 | $1,100,000 | $1,100,000 |

| Capital returned on refinance | N/A | ~$160,000 | ~$240,000 |

| Net capital left in deal | ~$250,000 | ~$200,000 | ~$150,000 |

The turnkey option gets you into a cash-flowing property fastest and with the least complexity. The value-add options require more upfront and more work, but they let you recover capital through refinancing and generate a higher return on the money that stays in the deal.

Neither approach is better for everyone. The right one depends on your income, your time, your risk tolerance, and what the market is offering right now. You can model both scenarios using our total return projections calculator to see how each one performs over your hold period.

Other Factors That Affect How Much You Need

The numbers above cover the most common scenario: a straight investment purchase with 20% down. But a few other factors can shift the capital requirement in either direction.

If you plan to live in one of the units yourself, you may qualify for a smaller down payment and a larger loan, depending on your income and the property type. That can bring the total cash you need down noticeably compared to a pure investment purchase. Toronto’s multiplex zoning rules have also expanded in recent years, which means more properties now qualify for conversion or addition of units. Understanding what is possible on a given lot affects both renovation costs and the upside you can create. Some properties may also qualify for additional units through garden suites or laneway suites, which changes the value-add math entirely.

Mortgage qualification is the other big variable. The bank needs to be comfortable lending you the amount required based on your income and existing debt. If you are not sure where you stand on this, it is worth sorting out early. There is no point falling in love with a deal if the financing does not work. The other key piece is knowing what your actual investment goals are — cash flow now, equity growth over time, or a combination of both. That shapes which properties make sense to pursue and what kind of deal you should be targeting.

Ready to Run the Numbers on a Real Deal?

Toronto multiplexes do not require the kind of capital most people assume. With the right property and the right strategy, $250,000 gets you into a cash-flowing asset in this city. And if you are willing to take on a value-add project, you can often recover a large portion of that capital through a refinance once the work is done.

The harder part is not finding the money. It is knowing which properties are actually worth buying, what the renovation will realistically cost, and whether the numbers hold up under honest scrutiny. That is where having an experienced team around you makes a real difference.

Our brokerage specializes in Toronto multiplexes. We’ll help you find deals, crunch the numbers, and guide you through renovations and management. If you want full support in Toronto multiplex investing, our team can help you:- Find high-potential properties

- Crunch the numbers so you know exactly where you stand

- Coach you through renovations to maximize returns

- Lock in great tenants

- Provide full property management so your investment runs smoothly

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.