When most people think about making money in real estate, they think about selling. You buy a property, it goes up in value, you sell it, you pocket the difference after fees and taxes. Simple enough. But that exit costs more than most people realize.

There is another exit strategy that a lot of investors do not talk about as much, and in many cases it is the better move. It is called BRRRR. The reason it is worth knowing comes down to one thing: lower costs to get your money out.

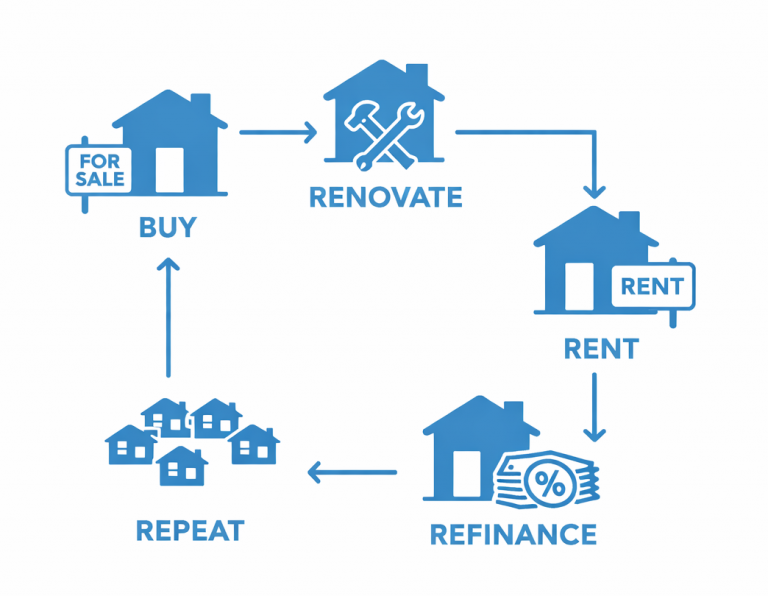

What Is BRRRR and How Does It Work

BRRRR stands for Buy, Renovate, Rent, Refinance, Repeat. You buy a property that needs work, renovate it, get it rented at stronger rents, and then go back to the bank and refinance based on the new higher value. The bank lends you more than your original mortgage, and that difference comes back to you as cash. You keep the property, keep the rental income, and use that cash to go do it again.

When you sell a property, you are paying real estate commissions, closing costs, and depending on how the property is structured, potentially a significant tax bill. That eats into your return fast. With BRRRR, you are not selling. You are pulling your money out through a refinance instead, and a refinance does not trigger the same costs.

The result is that more of your capital stays working for you. You are not giving a chunk of your equity to the government or to transaction costs every time you want to move money into the next deal. That compounding effect is what makes BRRRR one of the most efficient ways to scale a Toronto multiplex portfolio. For a full breakdown of how total returns stack up, use our total return projections calculator.

How the Refinance Actually Works

The bank orders an appraisal. The appraiser looks at what similar properties nearby have sold for and estimates the current market value. The bank will typically lend up to 80% of that new value. The gap between your original mortgage and the new loan amount comes back to you as cash.

Here is a simple example. You buy a triplex for $1 million and put $200,000 into renovations. After the work is done and the units are rented at stronger rents, the property appraises at $1.4 million. The bank lends you 80% of that. If your original mortgage was $800,000, that refinance puts roughly $320,000 back in your hands. That is a significant portion of your renovation budget back, without selling the property and without a large tax event.

You still own the building. You still collect rent every month. And now you have capital to go find the next deal. One important note for today’s market: appraisals have been coming in more conservative because of current buyer’s market conditions. That is not a reason to avoid the strategy, but it is a reason to build in a buffer when you are running the numbers upfront.

| Commercial Value | = |

|

Residential vs Commercial Refinance: What Changes at Five Units

On a residential property of one to four units, the bank values the property based on what similar homes nearby have sold for. Your ability to qualify for the refinance is based on your personal income, including your salary, rental income, and business income. As long as you qualified for the original purchase mortgage, you should be able to qualify for the refinance in most cases, especially since your renovations should have improved the rents.

Once you get to five units or more, everything shifts. Lenders treat it as a commercial property. They do not care what the house next door sold for. They value the building based on the income it produces, divided by something called a cap rate. If you renovate the units and push the rents up, the building generates more income and the value goes up directly as a result. That is a powerful dynamic when you are on the right side of it.

The trade-off is that commercial refinances are more sensitive to market conditions. Most investors doing larger projects are using CMHC MLI Select financing, which is tied to CMHC policy that has been tightening. On top of that, cap rates have been creeping up and rents have softened, which means commercial refinance valuations have been coming in lower than originally projected. That is part of why a lot of multiplex investors are shifting back toward residential projects right now.

Why Residential BRRRR Is Producing the Best Risk-Adjusted Returns Right Now

Residential multiplexes offer more predictable valuations, shorter timelines, and less capital at risk compared to larger commercial projects. You are also not exposed to the same CMHC mortgage policy risk. For most investors right now, that combination is hard to beat.

Turnkey deals are one place where the numbers are working well. A stabilized triplex in Toronto sells for around $1.2 million and requires roughly $300,000 all-in for the down payment and closing costs. Because prices have adjusted, you can still get over $1,000 per month in positive cash flow in today’s market. These properties used to not cash flow at all, so that is a meaningful shift.

Smaller value-add deals are another strong option. Buy around $1 million, spend roughly $50,000 on improvements over a few months, increase the rents, and the property could be worth around $1.1 million. That is approximately $50,000 in added value without taking on a major construction project. You improve the property, increase the income, and position yourself for a refinance later. Smaller value-add Toronto multiplexes are producing some of the best risk-adjusted returns available right now.

| Turnkey Multiplex | Small Residential Value-Add Project | Large Residential Value-Add Project | |

|---|---|---|---|

| Purchase | $1,200,000 | $1,000,000 | $800,000 |

| Construction Cost | $0 | $50,000 | $200,000 |

| Completion Value | $1,200,000 | $1,100,000 | $1,200,000 |

| Lift | $0 | $50,000 | $200,000 |

| Initial Capital | $282,000 | $285,000 | $388,000 |

| Cash Out on Refinancing | $0 | $80,000 | $320,000 |

| Construction Period | 0 | 2 months | 6 months |

Start Building Your Toronto Multiplex Portfolio

The BRRRR strategy works because it keeps your capital moving without the cost of selling. In Toronto’s current market, residential multiplexes are producing the most consistent results, with predictable appraisals, manageable timelines, and real cash flow from day one. The math on both turnkey and smaller value-add deals is better than it has been in years.

But the strategy only works if the numbers are right from the start. The purchase price, the renovation budget, the projected rents, and the refinance assumptions all need to line up. Getting any one of those wrong can turn a good-looking deal into one that does not perform. That is where having experienced support on your side makes the difference.

Our brokerage specializes in Toronto multiplexes. We’ll help you find deals, crunch the numbers, and guide you through renovations and management. If you want full support in Toronto multiplex investing, our team can help you:

- Find high-potential properties

- Crunch the numbers so you know exactly where you stand

- Coach you through renovations to maximize returns

- Lock in great tenants

- Provide full property management so your investment runs smoothly

Book a strategy session with us here and let’s map out the smartest move for your portfolio.

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.