Most Toronto investors pick their first investment property based on price. A condo at $500,000 feels safer than a multiplex at $1,000,000. Less money down, less exposure, easier to get into. That logic makes sense on the surface. But it ignores one thing: whether the property actually helps you grow.

If your first investment property loses money every month, it is not a stepping stone. It is an anchor. This post breaks down why the order you buy in Toronto real estate matters, why a cash-flowing multiplex puts you on a better path than a condo, and how the right first property can fund your second one.

Why a Cash Flow Negative Condo Hurts Your Next Deal

Banks do not lend based on what you hope a property is worth in ten years. They lend based on your income and your debt load today. If your investment property is losing $500 a month, that shortfall shows up on your debt service ratios every time you apply for a mortgage. Your borrowing capacity shrinks. Your savings are thinner. And the conversation with the lender for deal number two is harder than you expected.

Many Toronto condos are cash flow negative right now. The rent does not cover the mortgage, condo fees, and property taxes combined. Every month, the gap comes out of your pocket. Over five years at $500 a month, that is $30,000 out of pocket, plus weaker debt ratios, plus whatever appreciation you are hoping for. You own a property on paper. But financially, it is working against you.

This is the condo trap. It catches a lot of first-time investors who focused on the purchase price instead of the monthly numbers. The cheaper entry point feels like lower risk. But a property that costs you money every month is not lower risk. It is a slower version of the same problem.

What Multiplex Investors Can Do That Condo Owners Can’t

Most condo owners are passengers. You cannot add a unit. You cannot meaningfully increase rents across multiple doors. You cannot do much to the property to make it worth more. You are fully exposed to whatever the market decides to do, and in a flat or slow market, the market may not cooperate.

With the right Toronto multiplex, you have options. You can renovate units as tenants turn over and bring them up to a higher standard. A nicer property commands a higher price when buyers compare it to everything else on the street. That lift comes from what you did, not from what the market did. That is a fundamentally different position to be in as an investor.

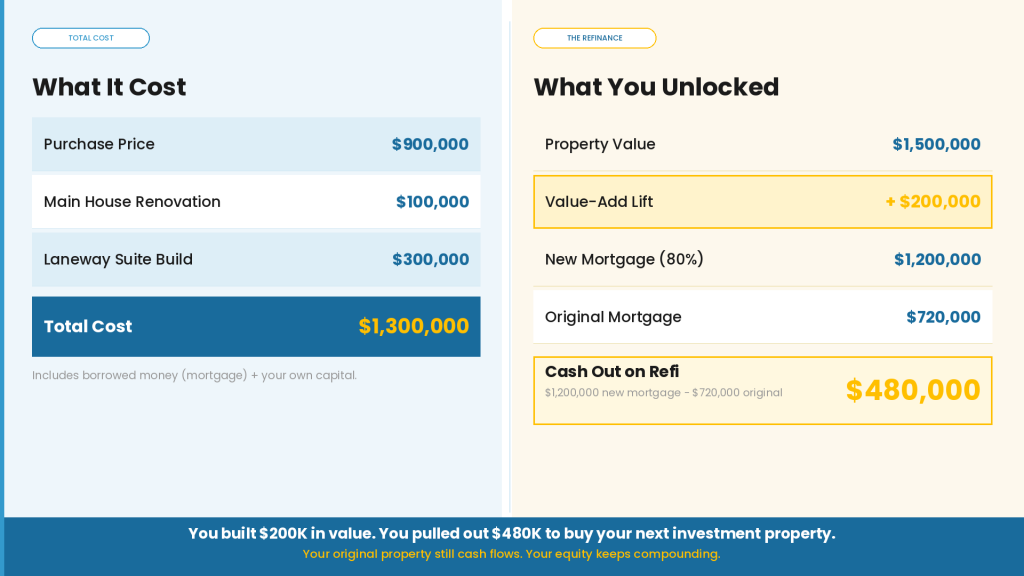

Toronto also has strong rules around laneway suites and garden suites. A lot of lots south of Eglinton qualify. Add a laneway or garden suite and you create a new income stream, build more equity, and improve your position when you refinance. That extra income and equity can help you pull capital out of the property to fund your next purchase, without selling anything. That is a strategy a condo will never give you access to. To understand which properties qualify, see our full guide on Toronto multiplex and sixplex rules.

What Multiplex Investors Can Do That Condo Owners Can’t

Most condo owners are passengers. You cannot add a unit. You cannot meaningfully increase rents across multiple doors. You cannot do much to the property to make it worth more. You are fully exposed to whatever the market decides to do, and in a flat or slow market, the market may not cooperate.

With the right Toronto multiplex, you have options. You can renovate units as tenants turn over and bring them up to a higher standard. A nicer property commands a higher price when buyers compare it to everything else on the street. That lift comes from what you did, not from what the market did. That is a fundamentally different position to be in as an investor.

Toronto also has strong rules around laneway suites and garden suites. A lot of lots south of Eglinton qualify. Add a laneway or garden suite and you create a new income stream, build more equity, and improve your position when you refinance. That extra income and equity can help you pull capital out of the property to fund your next purchase, without selling anything. That is a strategy a condo will never give you access to. To understand which properties qualify, see our full guide on Toronto multiplex and sixplex rules.

Condo vs. Multiplex: What Five Years Actually Looks Like

Two investors start at the same time in the same city. Investor A buys a Toronto condo. It loses $500 a month. Over five years they spend $30,000 covering the shortfall. Their debt ratios are weaker. Their savings are thinner. When they go back to the bank, the conversation is harder. They might still get the next deal, but it takes longer and costs more.

Investor B buys a Toronto multiplex. It generates $1,000 a month in positive cash flow. Over five years they collect $60,000. Their debt ratios are stronger because the rental income supports their application. They have reserves. And the property itself has appreciated in a market where well-maintained income properties hold value. When they go back to the bank, the conversation is easier and they have more options.

That is a $90,000 swing in cash position over five years, before you account for any difference in debt ratios or refinancing potential. One investor owns a property. The other is building a portfolio. Same city, same market, different starting decision.

Using Your First Toronto Property to Buy Your Second

Cash flow creates options. When a property pays you every month, you build reserves faster. Those reserves become your next down payment. The income from the property also strengthens your debt service ratios so you qualify for the next mortgage more easily. The first property becomes a tool for the second one, not a weight you are carrying.

Add a laneway or garden suite to the picture and the options get even stronger. A new unit adds rental income, which adds equity, which improves what you can pull out on a refinance. Some Toronto investors use exactly this approach: buy a multiplex, add an ADU, refinance at the higher value, and use the cash out to fund the deposit on the next deal. The original property still cash flows. The equity keeps compounding. This is what building a portfolio actually looks like in practice.

If your goal is simply to own real estate, a condo might get that done. But if your goal is to build a portfolio, reach financial independence faster, and use your first property as a launchpad, cash flow is not optional. It is the whole foundation. And in Toronto, where deals require real capital and real qualification, you cannot afford to spend five years learning that lesson on a property that was always working against you.

Ready to Find a Toronto Multiplex That Works for You?

The gap between owning one property and building a real portfolio usually comes down to one early decision. Buying something that cash flows, with value-add potential, in a market you understand changes everything that comes after. In Toronto, those deals exist. But you need to know where to look and how to run the numbers before you commit.

Our team works exclusively in Toronto multiplex investing and we are investors ourselves. We do not just transact on properties. We help you figure out the right strategy for where you are, and then we connect that strategy to the right deals.

Our brokerage specializes in Toronto multiplexes. We’ll help you find deals, crunch the numbers, and guide you through renovations and management. If you want full support in Toronto multiplex investing, our team can help you:- Find high-potential properties

- Crunch the numbers so you know exactly where you stand

- Coach you through renovations to maximize returns

- Lock in great tenants

- Provide full property management so your investment runs smoothly

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.