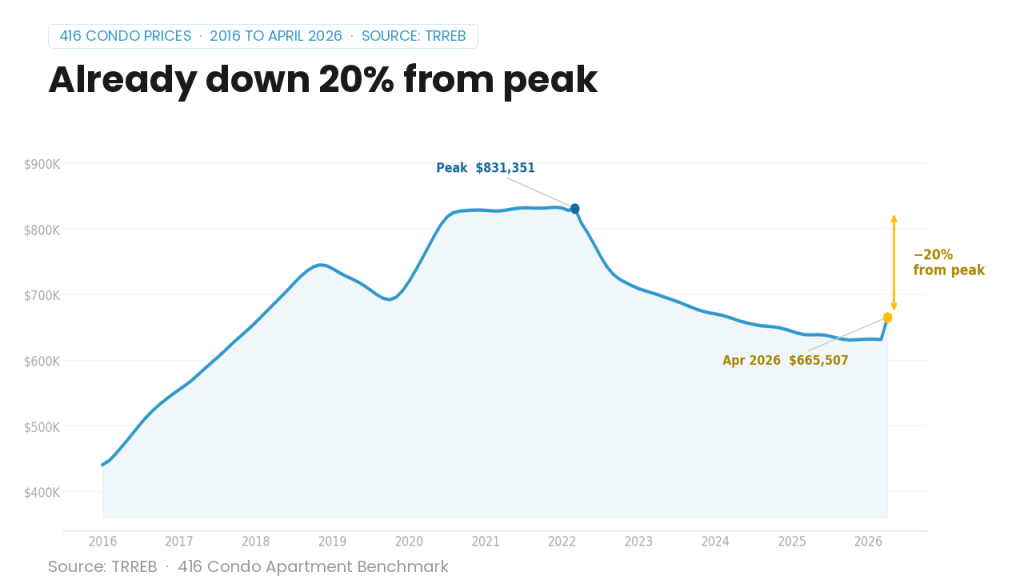

Toronto condo prices have already fallen 20% from their peak. On paper that sounds like a buying opportunity. But run the actual numbers on a typical two-bedroom and you are still losing over $1,000 every single month. That is not a buying opportunity. That is a trap with a discount sticker on it.

For a Toronto condo to just break even on cash flow — meaning you stop losing money every month — prices would need to fall another 40% from today. That would take them all the way back to 2015 levels. A total drop of over 50% from peak. That has never happened in Toronto real estate history. And even if it somehow did, we still would not buy one. Here is exactly why, and what the math says you should be doing instead.

The Cash Flow Math on a $750,000 Toronto Condo

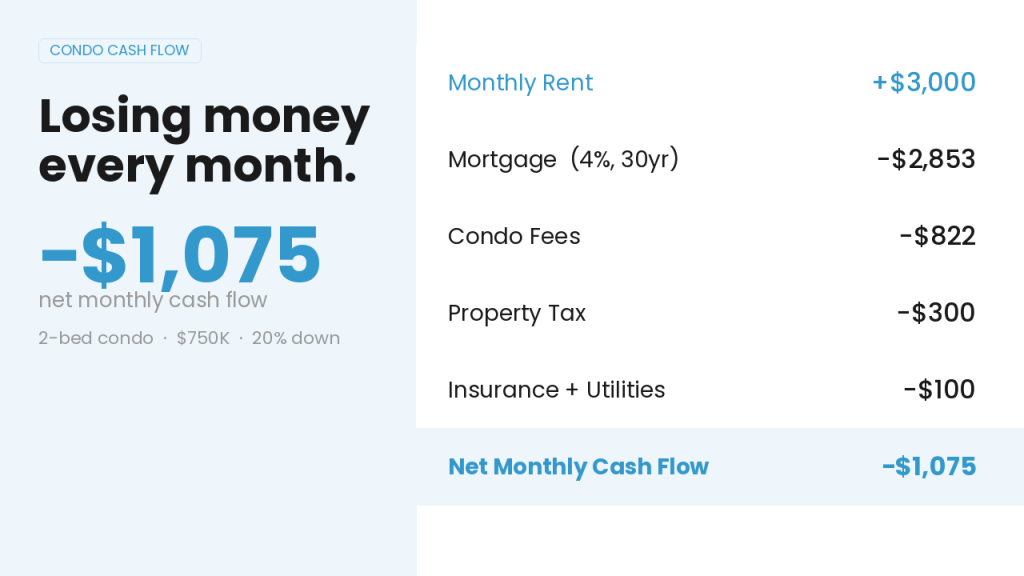

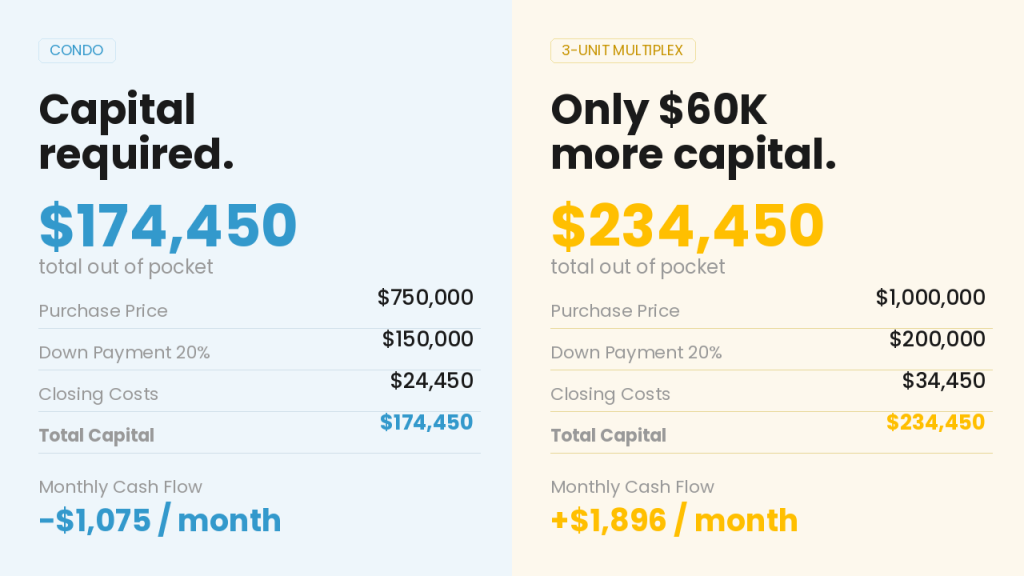

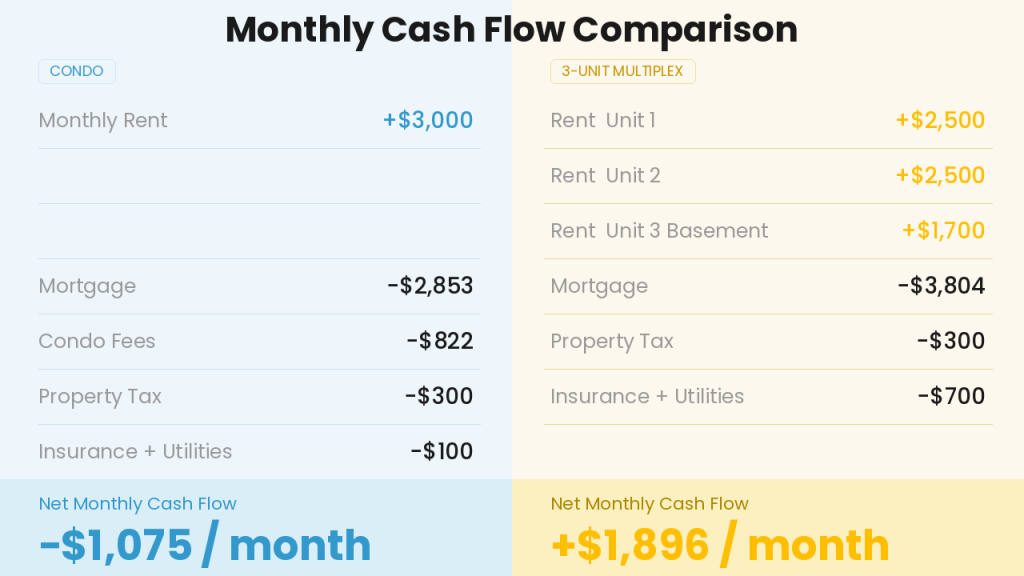

A decent two-bedroom condo in Toronto right now costs around $750,000. That is already about 20% below the peak. Put 20% down, factor in closing costs, and you are looking at roughly $175,000 out of pocket to get in. You rent it for $3,000 a month, which is a reasonable number for a two-bedroom in a decent area. So far it sounds workable.

Then the expenses hit. Mortgage, condo fees, property tax, insurance, and utilities. When you add it all up, you are losing about $1,000 a month. Every month. On $175,000 of your own money sitting in that property. That works out to a cap rate on cost of roughly 2.8%. You can learn more about what that number means and why it matters in our cap rate guide here.

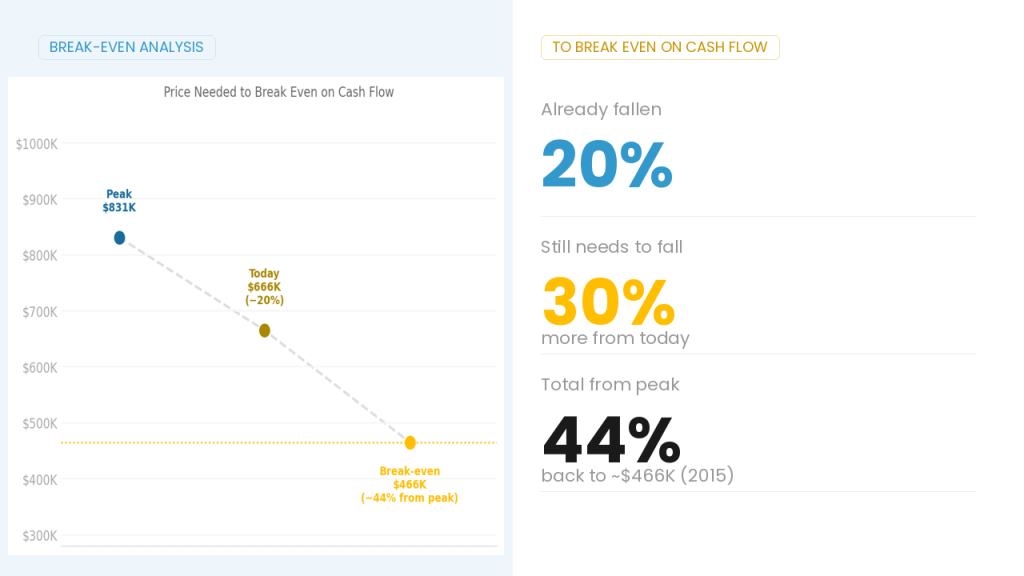

For the math to work — for the property to just break even — the price would need to fall from $750,000 to around $450,000. That is another 40% drop from today, on top of the 20% that already happened. In total you are talking about prices falling more than half from their peak. That takes Toronto back to 2015. The worst crash in Toronto history, back in 1989, only brought prices down about 30% before they recovered. Waiting for condos to get cheap enough to cash flow is not a strategy. That level of price correction has no historical precedent here.

Why Breaking Even Is Still Not Good Enough

Let’s say prices did fall to $450,000 and your condo finally broke even. You would still be getting nothing back on $175,000 of capital. Zero monthly income. Zero return on your down payment. You would just be treading water while dealing with tenants, condo fee increases, and a building that gets more expensive to maintain every year.

But here is the part that really hurts your long-term position. When you go back to the bank to buy your next property, they look at your existing debt load. A condo that is just breaking even shows no income coming in to offset the mortgage. That limits how much you can borrow. A break-even condo does not help you grow. It actively gets in the way.

Real estate investing is not just about whether a single property covers its costs. It is about whether it builds your ability to keep going. An asset that earns nothing, on a building you do not control, on land you do not own, with fees going up every year — that is not a foundation. That is a ceiling.

What $60,000 More Gets You: A Toronto Three-Unit Multiplex

For about $60,000 more out of pocket, you can buy a three-unit multiplex in a starter Toronto neighbourhood instead. Think pockets of East York or Corso Italia — properties trading around $1,000,000 right now. Total capital required, including closing costs, is roughly $235,000. That is the comparison: $175,000 into a condo that loses money, or $235,000 into something that makes money.

Here is what the income looks like on a typical three-unit. Two above-ground two-bedroom units renting at $2,500 each, and a basement one-bedroom at $1,700 a month. Total rental income: $6,700 a month. After the mortgage and all operating expenses, you are clearing close to $2,000 a month in positive cash flow. Before any appreciation. Before your tenants pay down your mortgage. You can run your own numbers using our total return calculator.

Now go back to the bank for your next property. Instead of showing a debt with no offsetting income, you are showing a property that earns. The bank sees that your portfolio is cash flow positive and your borrowing power grows. That is how you build a portfolio over time. The condo scenario keeps you stuck. The multiplex scenario keeps you moving.

Land Ownership, Value-Add, and the Long-Term Gap

When you buy a condo, you do not own land. You own one unit inside a building that ages every year. As it ages, maintenance costs rise, special assessments hit unexpectedly, and the condo corporation makes the big decisions — not you. When you buy a house, you own the land underneath it. Land in Toronto is finite. Families and investors both want it, and that steady demand protects your resale value in a way a condo building simply cannot replicate.

The value-add gap is just as significant. A condo is essentially a finished box. Even if you want to renovate, getting contractors in and out is complicated, building rules limit what you can do, and the upside on a freshened-up unit is marginal. With a house it is the opposite. Update the kitchens, bathrooms, and mechanical systems and you raise both the rents and the appraised value. The property responds to what you put in.

Toronto now also allows most property owners to build a garden suite or laneway suite on the same lot. A new unit built for around $350,000 can rent for $3,000 or more per month. That is close to a 9% rent yield on the construction cost alone. You cannot add a unit to a condo. You cannot expand it. You cannot build on it. The ceiling is built in from day one. For a full overview of what Toronto currently allows on multiplexes, see our Toronto multiplex and sixplex rules guide.

What to Do If You Already Own a Condo

A lot of investors we speak with have built up $200,000 to $300,000 in equity in a condo that is costing them money every month. That equity is not doing nothing — but it is not doing much either. It is sitting in an asset that has negative cash flow, limited growth potential, and no land backing it up.

That equity could be redeployed into something that pays you monthly, improves your borrowing position, and gives you actual options to grow. It is not automatically the right move for everyone. There are tax implications to selling, so the first conversation should be with your accountant. But if you have been holding your condo and quietly hoping the market turns around, it is worth doing that math honestly before another year passes.

The condo thesis — that 10% annual appreciation would cover monthly losses — is not working anymore. Prices have already fallen significantly from peak. The carrying costs are still real. The land ownership gap, the borrowing power gap, and the value-add gap have not closed. If your equity is trapped in an asset that is working against your next move, that is worth addressing sooner rather than later.

Ready to Put Your Capital to Work?

The numbers here are not abstract. A typical Toronto two-bedroom condo at $750,000 is losing over $1,000 a month after expenses. For it to break even, prices would need to fall another 40% — a level Toronto has never seen. And even at break even, the asset still loses on land ownership, borrowing power, and future growth potential. For roughly $60,000 more in capital, a Toronto three-unit multiplex flips that equation: close to $2,000 a month in positive cash flow, a stronger mortgage qualification position, and real options to grow the value over time.

That gap does not close by waiting. It widens. Right now, buyers have real leverage — conditions, inspections, time to get contractor quotes, and room to negotiate a price that actually makes sense before you sign anything. If you are holding condo equity that is not working, or you are ready to move into multiplex investing with a team that knows the Toronto market, the time to run the numbers is now.

Our brokerage specializes in Toronto multiplexes. We’ll help you find deals, crunch the numbers, and guide you through renovations and management. If you want full support in Toronto multiplex investing, our team can help you:- Find high-potential properties

- Crunch the numbers so you know exactly where you stand

- Coach you through renovations to maximize returns

- Lock in great tenants

- Provide full property management so your investment runs smoothly

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.