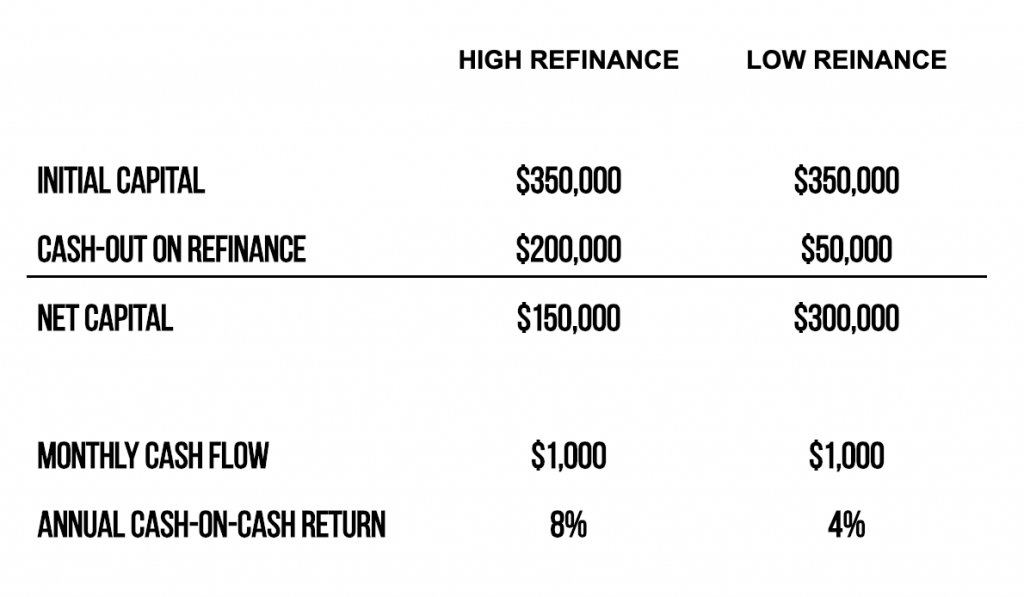

Same renovation. One investor pulls out $300,000 at refinance. The other pulls out $150,000. The difference is not the work they did. It is how they understood the appraisal process before they started. If you are doing a BRRRR on a Toronto triplex or fourplex, this is one of the most important things to get your head around.

Most investors assume more units means more value, or that strong rents will push their appraisal higher. Neither is reliably true for small multiplexes in Ontario. The rules that govern how your property gets valued are different from what most people expect, and once you understand them, you can position your deal to pull out as much capital as possible and move on to your next property sooner.

Why Small Multiplexes Are Valued Like Houses, Not Apartment Buildings

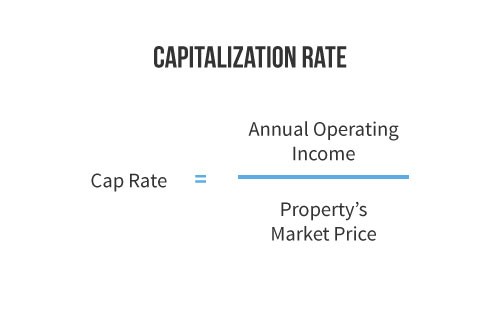

In Canada, the number of units in a property determines which valuation method a bank applies. Five units and up is typically treated as commercial. When a lender looks at a commercial property, value is driven by income. The more rent the building generates, the higher its value. That is where cap rates come in.

Under five units — your duplex, triplex, or fourplex — the bank treats the property like a regular house. That means the appraiser is not primarily looking at how much rent you collect. They are looking at what comparable properties on your street have recently sold for. What did the house next door sell for? How does yours compare? Those sales are what drive your appraised value.

Your rents do not move your appraised value in the same direct way. Rental income matters when you apply for the mortgage, because a lender wants to see that the property generates income before they approve your borrowing. But the value on paper, and the number the refinance is based on, comes from the sales comparison approach. Understanding that distinction is the foundation of everything else.

What an Appraiser Actually Looks at When They Walk Through Your Property

The first thing an appraiser considers is the type of property. Detached or semi-detached? One storey or two? How large is the lot? These factors determine which nearby sales they can use as comparables. A detached house will almost always appraise higher than a semi-detached on the same street, even if both collect the same rent. The building type sets the starting point, not the number of units.

Condition and finishes matter more than most investors expect. A well-renovated two-unit can appraise higher than a three-unit with average finishes in the same neighbourhood. The appraiser is comparing your property to what buyers have been willing to pay nearby, and a polished, move-in-ready property commands stronger comps than one that just has more doors.

The number of units does help when it comes to your mortgage qualification. Documented rental income from additional units can allow you to borrow more at refinance. Some lenders require legal status before they will count that income. Others are more flexible. Your mortgage broker should be checking multiple lenders, because what one declines, another will often approve without hesitation. Do not assume one answer applies everywhere.

Why the Neighbourhood You Buy In Shapes Your Refinance Before You Even Start

The neighbourhood your property is in determines which sales the appraiser can draw from. Not all neighbourhoods produce the same appraisal outcomes for the same renovation work. This is one of the factors investors most often overlook when they are sourcing deals.

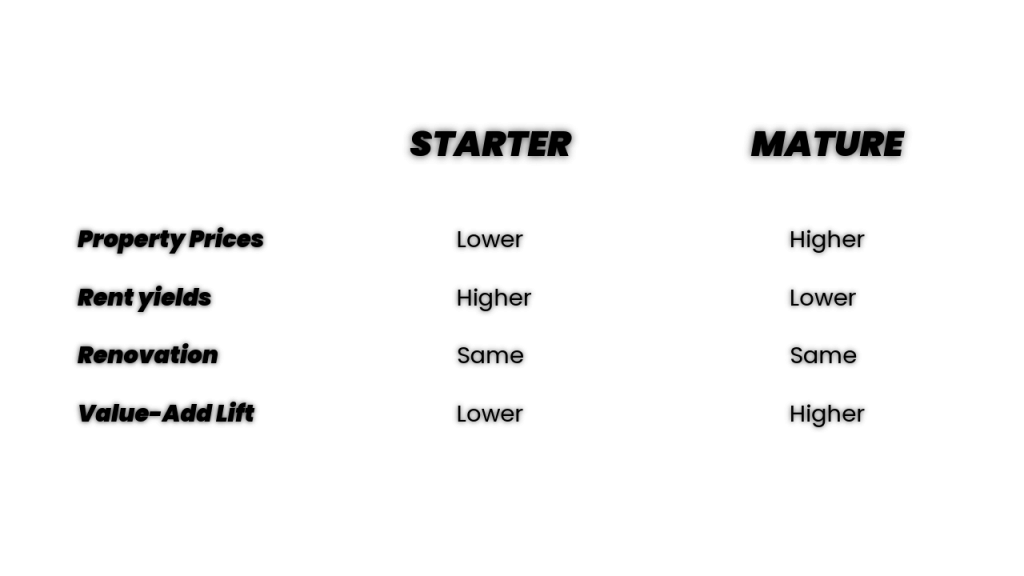

Areas with stronger rent yields in Toronto often come with lower purchase prices, and that means appraised values are typically lower as well. In contrast, neighbourhoods where families are actively buying homes tend to have a bigger spread between properties that need work and those that are move-in ready. Buyers in those areas are paying for the street, the school nearby, and the overall feel of the area. When an appraiser looks for comps there, the finished homes command meaningfully stronger numbers.

What this means in practice is that the same renovation budget, applied to a property in a higher-demand family neighbourhood, is likely to produce a stronger appraisal lift than the same work done in a lower-price area. Where you buy shapes how much you pull out. Factor this into your acquisition analysis before you make an offer, not after you finish the renovation.

How to Prepare for the Appraisal and Why It Changes Your Result

When the appraiser shows up, have a package ready for them. Include what you paid for the property, what you spent on the renovation, and a clear summary of exactly what work was done. Add before and after photos. Include any permits you pulled. Bring a selection of recent sales from the area, particularly family homes or properties with secondary suites that sold for strong numbers.

You are essentially doing part of their homework for them. An appraiser with clear documentation and recent supporting comps is in a much better position to justify a higher value than one walking into a finished renovation with no context. The ones who arrive prepared consistently walk away with stronger appraisals.

There is one more thing that sounds obvious but genuinely matters. Be courteous to your appraiser. They are exercising judgment within a range, and showing up with a well-organized package and a professional attitude makes it easier for them to arrive at the number your renovation supports. It is a small thing that costs nothing and can make a real difference to the outcome.

How the Appraised Value Drives Your BRRRR Returns and Your Speed to the Next Deal

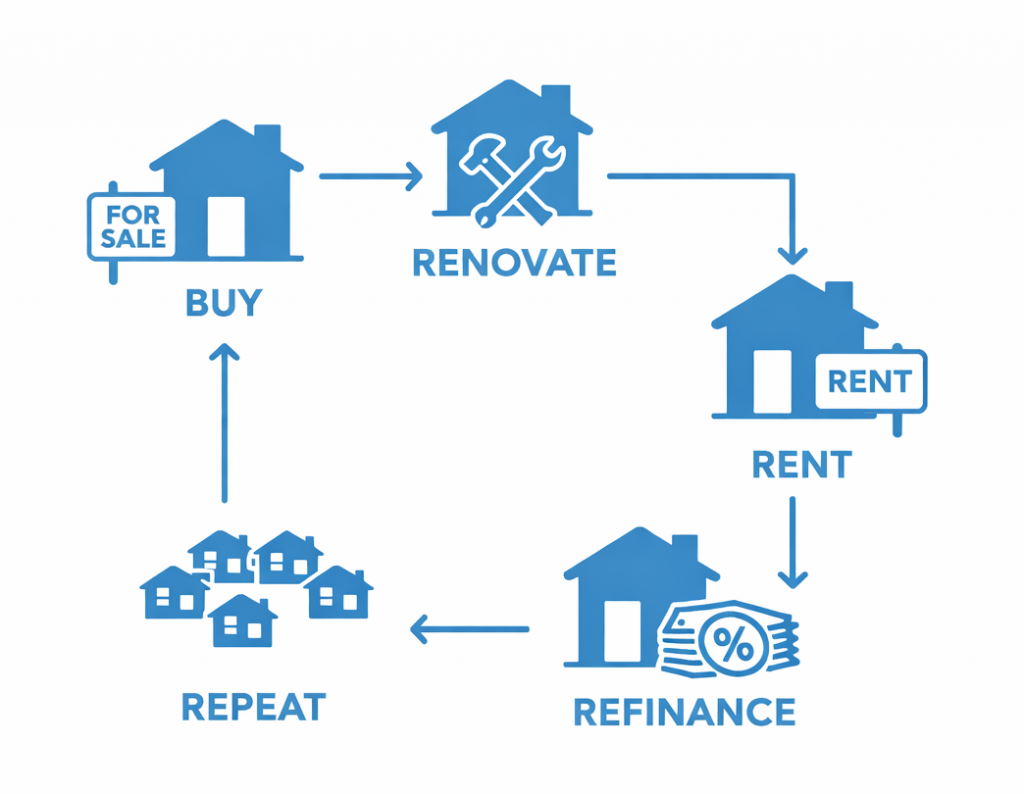

The whole point of the BRRRR strategy is to recover your capital so you can deploy it again. You buy, renovate, refinance, pull your money out, and repeat. The appraised value after your renovation is what determines how much capital you get back and how little of your own money stays tied up in the deal.

The difference between pulling out $300,000 versus $150,000 is not just the size of the cheque. It is how quickly you can move on to the next property, and how your return looks on the capital that remains in the deal. A property generating $1,000 a month in net cash flow looks very different when you have $150,000 tied up versus $300,000. You can use the total return calculator to model exactly how much your equity position affects your overall return.

If you are focused on building a portfolio of Toronto multiplexes, the appraiser is one of the most important people in your process. Understanding what they look at, buying in the right neighbourhood, preparing properly before they arrive, and working with a mortgage broker who knows how to position your income documentation — these are the levers that determine how fast you scale. The renovation is table stakes. The appraisal outcome is what lets you move.

Work With a Team That Knows How Toronto Multiplexes Get Valued

Getting the most out of a BRRRR comes down to decisions made well before the renovation starts. The neighbourhood you buy in, the type of property you target, the documentation you bring to the appraisal — all of it adds up to the number on the refinance and how much capital you walk away with. If you get that part right, the strategy works the way it is supposed to.

At Elevate Realty, we work with investors who are building Toronto multiplex portfolios and want to do it efficiently. We help you find the right properties, run the numbers before you buy, plan renovations that move the needle on value, and support you through the refinance when the time comes.

Our brokerage specializes in Toronto multiplexes. We’ll help you find deals, crunch the numbers, and guide you through renovations and management. If you want full support in Toronto multiplex investing, our team can help you:- Find high-potential properties

- Crunch the numbers so you know exactly where you stand

- Coach you through renovations to maximize returns

- Lock in great tenants

- Provide full property management so your investment runs smoothly

What Toronto Real Estate Investment Is Right For You?

Check out our complete Toronto real estate investment guide for all the details and real-life examples. If you’re ready to dive in, just book a call with us!

This is for educational purposes only; it does not guarantee future performance or serve as financial or tax advice.